Author: Clinton Waters

Proudly supporting the Young Pink Sisters charity

Axton Finance wins at Connective’s Level Up Conference

We are very proud to announce that Axton Finance won Connective’s Brokerage of the Year <5 Staff VIC. Thank you to our great team and clients who supported us over the past 12 months. Contact us here or ring on 03 9939 7576 for all your mortgage and finance requirements.

Receiving a windfall

Guest blog content written by Corey Wastle – Licensed Financial Adviser @ Verse Wealth

Most people will at some stage in life receive an unexpected amount of money.

It might be a gift, work bonus, lottery win or more commonly an inheritance.

These ‘windfalls’ are often used to pay down the mortgage and relieve financial stress. They also often will allow people to take on the projects they’ve always put off until ‘I have the money’.

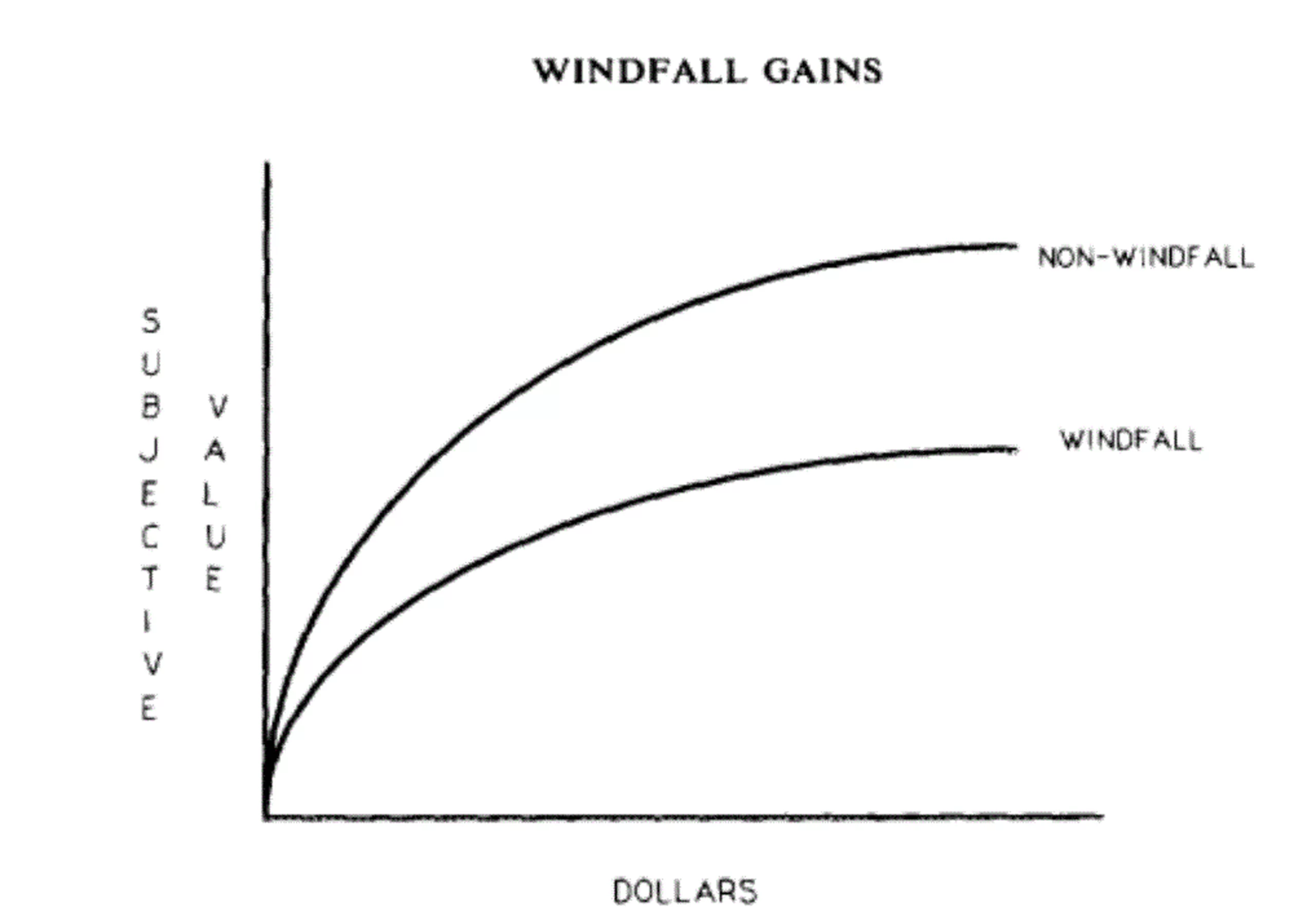

It’s a time of great opportunity however it can also be a time for careless expenses and poor decision-making. In fact, a large number of studies like this one show that windfall gains are spent far more readily than when effort is exerted to earn the money. These studies illustrate that when it comes to our perception of the value of the dollar, not all money is equal.

Windfall payments are often coupled with a spike in living costs. One-off expenses like new cars and international holidays, increase significantly. This happens because an unexpected lump-sum can be hard to contextualise against the money that we’ve always had to work so hard for. A large payment with no context is a very dangerous combination and it’s common to make some of our biggest financial mistakes during this time.

Fortunately, there are steps you can take to reduce the likelihood of making a serious (or series) of financial blunders after receiving a windfall. Here’s a few of our suggestions:

Find your baseline: Have a sound understanding of your weekly or monthly expenses and keep them unchanged until you’re ready to do something with the windfall. A quick or even steady rise in your expenses will see that precious money diminish faster than you thought possible. If you don’t already know your expenses, complete a budget planner to learn what they are.

Need vs Want: One of the most important questions to ask when making any big purchase is, ‘Do I need this, or do I want this?’ Regardless of your situation, ‘needs’ always come before ‘wants’. If you identify that you might not need the item, take the time to think about any things which you do need before spending your money on the wants.

Get ahead: Let’s cut to the chase – it’s not easy to get ahead when you’ve got a mortgage, kids, bills and little time. If you’ve been fortunate enough to receive a windfall, make sure that all or part of this money is used to move you closer to financial freedom. This will generally mean that you’re paying down debt or purchasing quality long-term investments, or even both. Don’t squander a rare opportunity. They’re rare for a reason.

Consider alternatives: If you’re thinking about making a big purchase with this money, ask yourself what else you could spend the same amount of money on. The new car or renovation to an already nice home might seem like a good idea at first thought but hindsight may leave you questioning this later on. Would you or your family be happier doing something else with this money? It can help to chat to a friend or family member – simply talking through your options can go a long way to clarifying what is truly important to you.

Corey Wastle – Licensed Financial Adviser

Please Note: At AXTON Finance we work with a number of professionals and professional firms (we call them ‘Advice Partners’) to help ensure that anyone in the AXTON community gets all the advice they require to get financially organised, on track and achieving the things that really matter. We have invested countless hours to find the best in accounting, financial planning, estate planning, family law, commercial law and buyers advocates based on their expertise and commitment to the highest level of client care.

We do not take referral fees or receive commissions from of our Advice Partners.

Four smart questions to ask yourself when fixing your home or investment loan

1. Should I fix my home loan?

With interest rates at historical lows currently (at time of publishing there is a 3.99%pa (3) Three year fixed home loan rate now available from a major lender!!) many clients often ask me whether they should fix their home loan mortgage when buying or refinancing their properties. My response is always the same – fixing your mortgage is guaranteed peace of mind but not a guaranteed money saving exercise.

If you were taking on a rather significant amount mortgage that you were not absolutely comfortable with if your circumstances were to change then it may be worthwhile to fix a component of your debt. Doing so will provide you with certainty that no matter what happens to rates.

For almost every lender, bar one or two, you cannot generally pay more than the set repayments of a fixed rate mortgage – if you did you are usually limited to only about $10,000 per annum or less sometimes. Offset accounts are usually not allowed or calculated on a small percentage partial amount but you can choose at no extra cost to have principal and interest or interest only loans.

fixing your mortgage is guaranteed peace of mind but not a guaranteed money saving exercise.

2. How long should I fix for?

Well this is usually a simple matter of personal preference but from years of experience most clients generally fix for between two and three years – not only is this usually where the best fixed rates exist but it also provides a medium term structure of certainty for most clients.

3. Will I pay more if I fix?

Again this is usually a function of what term you decide to fix for – generally speaking the longer the fixed term the more expensive the rate becomes . This is because banks and lenders price their fixed rate mortgages on the basis of future expectations. At the time of writing this piece (April 2015) home loan rates have been at historical lows.

4. How much should I choose to fix?

Almost all lenders will enable you to fix a portion of your home loan based on almost any percentage you wish. A good yard stick is 50/50, 60/40, 70/30 fixed and variable respectively. Another good question to ask your self how much do you think you could pay off the variable loan during the initial fixed term – are there any windfalls or lump sums that you may be expecting?

If its all too hard to make a decision now or you think that rates are likely to drop further then you can also usually settle your loan as being variable and choose to fix at a latter stage. Depending on the lender there may be a small maintenance fee to do this depending on the product and package you are on.

Of course should you have any questions please feel free to myself Clint Waters at AXTON Finance Hawthorn East on 1300 706 540 or [email protected]

Reduce your mortgage insurance premium

There is no denying it – mortgage insurance or lenders mortgage insurance (LMI) kind of sucks.

This short article is about ways in which you can avoid mortgage insurance or at very least significantly reduce costs but first a few basic facts:

– It protects the bank not you

– It is a once off premium

– You have to pay it if your loan amount is greater than 80% of the property’s value

– The premium can often be added to the loan meaning you do not need to increase your cash deposit

– Getting a refund if your refinance these days is all but unheard of

– It can be expensive but you knew that right!

In the long term its often not as expensive as you may first think – especially if you have a strategy of paying off the loan sooner than the approved loan term (which everyone should try and aim for!). Paying one or two percent extra to buy a property sooner with a smaller deposit can often be recouped by paying today’s prices rather than delaying your purchase by a year or more and paying tomorrows prices which could be much more than the cost of the initial premium.

So how do you avoid or at least minimise paying lenders mortgage insurance?

Option One – Reduce your loan to valuation ratio

For almost all circumstances mortgage insurance kicks in once you borrow in excess of 80% of the value of your property. By increasing your deposit or reducing your purchase price you may be able to minimise the cost of the premium. A sure fire way to save money is to keep your lending under 90% of the value of the property – the moment you go above this threshold the cost of the mortgage insurance sky rockets (it can almost double in many instances). Call us to get a quote or tailored explanation of how it might apply based on your scenario.

Option Two – Use A Family Pledge

Your can eliminate the mortgage insurance cost entirely with the help from a family member who already owns property. This increasingly popular facility that we use is known as limited equity guarantee or a family pledge structure. Check out a detailed explanation of how this simple structure works here on our blog.

Option Three – Do you work in one of these industries?

Some of the banks offer packages that enable certain borrowers to lend up to 90% without paying any mortgage insurance. This is generally available for professionals in speciality industries such as lawyers, doctors, physios, dentists, sports stars and entertainers.

I hope this helps explain how mortgage insurance works in a little more detail. Please contact us here for an obligation free chat or ring 1300 706 540 to discuss your individual mortgage needs.

Get your home sooner when a family member guarantees part of your home loan.

Do your parents want to help you buy a home or invest in property?

Many lenders these days offer limited equity guarantee or family pledge loan structures to help you purchase a home without the absolute necessity of a cash deposit. Furthermore a family pledge structure will usually eliminate the need to pay expensive once off lenders mortgage insurance (LMI) costs.

How family pledge works?

Your family members (usually parents) can use their own home’s equity to provide additional security for a portion of your loan amount. This solution reduces your loan to value ratio and can also save you a significant amount of money by reducing or even avoiding the need to pay Lender’s Mortgage Insurance. So you get into your home faster, with help from your family.

With most lenders the guarantee can be limited to a specific amount (so not guaranteeing your full loan) which helps provide certainty and allows the property to be released much earlier than guarantees which cover 100% of the loan amount.

Benefits

- By increasing your security through a guarantee from your family, you may be able to reduce or avoid paying Lender’s Mortgage Insurance. Lender’s Mortgage Insurance is generally payable on loans that exceed 80% of the value of the property.

- A Family Pledge can help you maximise the amount you can borrow so you can purchase the property you want. A guarantor can request to limit the guarantee to a specific amount

- Both the borrower or guarantor can ask us to release the guarantee at any time once standard Loan to Value ratio (LVR) requirements are achieved (usually 80%)

- Interest rates and packages are the same for almost all Family Pledge loans. Standard guarantee and legal fees from most banks will normally apply.

- The guarantor can be a new or existing customer of the bank we recommend. The guarantor can even retain their home loan with their current Home Loan provider providing sufficient equity exists.

Take this example

Say you were planning to purchase a $500,000 property with a $25,000 deposit (ignoring closing costs for simplicity you would have a Loan to Valuation LVR of 95%), this would mean Lenders Mortgage Insurance (LMI) would most certainly be payable.

If your parents had a residential property and agreed to provide a family pledge guarantee of $75,000 as an additional security, your LVR would be reduced to 80% (this guarantee is not a cash loan but the lender does register their interest by way of a mortgage for the guarantee amount only against the guarantors property).

This would result in the LMI premium requirement being waived, up to a $17,760 saving for you (eg. 3.4% of the required 95% loan amount plus Victorian stamp duty of 10% using indicative QBE LMI rates as of Jan 2015)!

While this example uses a deposit some lenders do not require this and can approve a loan to valuation ratio up to 100% PLUS costs (stamp duty etc). This may result in an approval of up to 106% if required – we of course recommend a deposit is always preferable though.

Are you eligible for Family Pledge guarantee?

- You can use a Family Pledge to buy a home or invest in residential property, and you don’t have to be a first home buyer to be eligible!

- Family members who can provide the Family Pledge guarantee include parents, grandparents, siblings, sons and daughters.

- Family Pledge is generally not available for existing loans or refinances. Increases to loans with Family Pledge are allowed but the Family Pledge amount may not be increased usually.

- Individual applicants are restricted to a maximum of one parental guarantee/family pledge borrowing.

- As a rule of thumb no single guarantee is to represent more than 50% of the guarantor’s security. Some banks do not allow guarantees to be against a parents owner occupied home but only investments while other do not.

- Guarantors are usually required to secure independent financial and legal advice as a condition of loan approval.

- Family pledge loans can guarantee security only and NOT income (you must be able to earn sufficient income to service the entire loan based on your own resources).

Call us today to discuss your situation on 1300 706 540 or email.

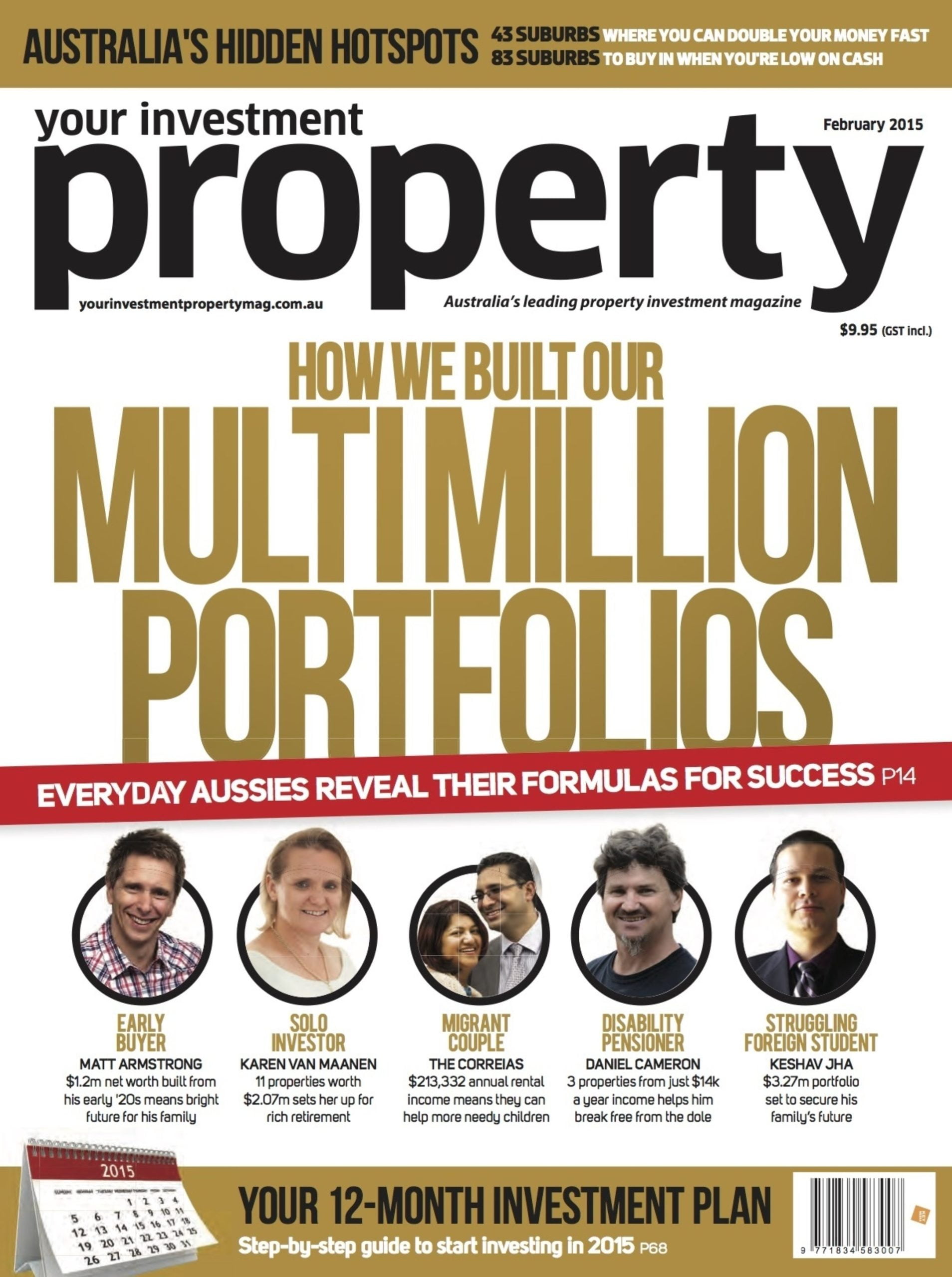

Axton Finance client wins property investor of the year

Your Investment Property Magazine recently announced their Property Investor of the Year Winner who is actually Axton Finance’s long term client Matthew Armstrong!

Matthew has built an impressive portfolio of five quality properties over a number of years. In the article Matt talks wisely about taking a long term approach to investment with some common sense tips on what makes a sound strategy. He also highlights the importance of getting a top team of professionals on his side which he lists as his mortgage broker (Matt did say he mentioned Axton but they edited us out!), buyers advocate, solicitor, accountant and property manager.

A big congratulations to Matt and his award – being such a modest fellow we had to find out about this from the magazine!

10 tips to paying off your mortgage sooner

I often joke with clients that I provide them with something they don’t really want – a mortgage. Lets face it – a mortgage in its own right isn’t too exciting but it enables your dreams to be realised. Those dreams might include a new home purchase, a renovation, buying a business, a new car – and the list goes on.

Fortunately, there are a few simple steps that you can implement to reduce your mortgage:

1. Pay Fortnightly

Yep, it’s that simple. Paying fortnightly saves about five years on your mortgage and it’s only because of the magic of compounding interest (but working in reverse). Paying fortnightly means you make the equivalent of 13 monthly repayments per annum – and that can make a BIG difference.

Make small but regular extra repayments – similar to fortnightly repayments. Combine the two and you really start turbo-charging your loan.

2. Bank Pre-Approval Limits

The amount a bank will lend a customer is staggeringly large, relative to people’s income. Just because you are pre approved and can afford today’s repayments, it’s important to think about what might happen if things change – higher rates, single income family, change in careers, unemployment etc. Even though a lender will sensitise repayments at 7-8% for ‘what if rates go up’, they use such measures as the Henderson Poverty Index to determine minimum living expenses for default family sizes – the key word here is ‘poverty’ – so if you like doing other things, like going out occasionally, keep well within bank servicing requirements. We can provide you with clear guidance on this important assessment to ensure taking on that mortgage doesn’t mean sacrificing other important areas of your lifestyle.

3. Got a raise recently?

Spend half and put the extra into your home loan – before you know it, if you don’t do this, the money you will make on the raise will be swallowed up in new lifestyle expenses in the blink of an eye!

4. Put your tax refund to good use

By putting a lump sum, like a tax refund, into your mortgage might sound boring but it can save you thousands! For example, on a new 30-year home loan of $500k, a $4,000 lump sum paid one year into the loan (with no other debt reduction strategy applied) could save you $10,580 and 5 months off the loan term.

5. Give your current bank the flick – Refinance

Refinancing your home loan, if there is a significant margin in interest rate to do so, could be a good idea. We usually give your current lender first right of refusal before we actually load a full application – if the difference is small in rate, then a full refinance may not be all that economical to do (find a competing bank branch who will tell you this small truth!!). If refinancing, it’s important to keep the repayments at the same amount to secure the same remaining term on the loan – it you refinance and take a new 30-year term on minimum repayments (which is what most people do without proper advice) then you will just reset your amortisation curve and any interest saving will be blown out of the water. (Ask us for a quote to demonstrate this – the findings will frighten you!)

6. Consolidate Debts

A bit like a refinance, except you may consider rolling your current loan, store cards and credit card into your home loan – but, again, tread with caution. I’ve seen many ads that advocate this and telling customers how they ‘saved’ hundreds in repayments but the reality is that if you consolidate and take a new 30-year term on minimum repayment the short-term personal debt (car loan, personal loan, etc) will be replaced with a long-term debt product (the mortgage) and the true cost will be eye-watering over the life of the loan- long after the current assets like the car, boat or TV bought on interest-free terms are gone.

7. Use an offset account

An old technique now but effective if you are not bad at budgeting. The premise with this is that you use the interest-free terms on the credit card and spend your monthly budgeted expenses using the card, while your salary and savings continue to sit in the offset account. At the end of the month, the credit card is automatically swept (paid) and you will have benefited from reducing your interest bill slightly for the month. This does have a compounding effect and can be very effective but it does require some budgeting skills and you also need to be careful that you don’t spend more than you earn by using the credit card. If the card is not paid in full by the due date, most credit card companies will slog you the full month’s interest on the amount you spent – so be careful!

8. Budgeting

Ok don’t yawn but a budget really can make a huge difference in where you spend your money. A great app that can help make budgeting easy and the above offset tip work more effectively is as Australian app called Pocket Book. It automatically takes a feed of your expenditure and summarises it all into a simple automated budget planning tool – it’s super nifty!

9. Downgrade

Some family homes are just simply too big now that kids have grown up or moved out. We can help determine an approximated end debt position with a relocation worksheet that could simulate what sort of mortgage you might have (if any), if you choose to do this after all considered costs.

10. Carve it up

Do you really need such a big back yard? Speak to a builder or a town planner to see if you could carve off the back yard and build a townhouse or a granny flat in the back. Subject to council planning and building requirements, this can make a huge dent in your home loan if you decide to build and sell a unit in the back yard or hold and keep as investment for the medium to long-term.

So there you go – 10 simple yet effective ideas to help you get ahead on your mortgage.

Please contact us here if you would like any advice on your mortgage reduction strategies today or ring now on 1300 706 540.

Are you an Australian Expat?

Over the years I have helped countless Australian expat clients working in all corners of the world to appropriately finance their property portfolio back here in Australia.

Building your property portfolio with tailored mortgage advice

With the advent of new technologies, expat acquisition of property in Australia has become significantly easier. By getting in touch with me and using various simple yet powerful tools on the internet you can gain easy access to our experience and expertise. We offer packaged mortgage broking and portfolio structuring advice encompassing:

– Purchase of owner occupied home and investment properties

– Owner occupied purchases or refinances

– Lines of credit establishment for investment purposes

– Property portfolio planning

– Mortgage health check reviews

Where initial face-to-face meetings are not possible, I can conduct client meetings via SKYPE video (see my availability & book obligation free skype meeting here) and I will provide you with much more than just an opinion of a rate and product offered by a bank. I provide a live shared screen viewing of proposed structures and worksheets especially tailored to your individual circumstances.

Quick Facts for Australian Expat mortgages

– Expats can generally borrow up to 90% of the value of the property purchased

– Some professions are eligible for the waiver of mortgage insurance if lending >80%

– No loading on interest rates – normal resident discounts apply

Interviews can be completed on SKYPE

– Foreign Currency Loans (FCL) available in certain circumstances

Private banking solutions available

Get access to our network of trusted professionals:

Over the years I have established trusted relationships with some of Melbourne’s best professionals who you too can confidently leverage upon without having to trawl the internet remotely trying to find the right people to help you with your property needs.

We have direct access to leading professionals in the following fields:

Buyers advocates – where clients are not able to inspect or bid for a property in Australia, a buyers advocate can source and review properties and negotiate on your behalf. Our advocates have years of experience and can help ensure clients make the right decision with the confidence as if they were undertaking the transaction themselves.

Solicitors/conveyancers – aside from arranging the settlement and legal transfer of real estate into a client’s name, it is vital that property contracts and disclosure documents (known as section 32’s in Victoria) are closely examined to identify any hidden pitfalls. Our preferred conveyancers are experts at assuring a smooth settlement process and identifying issues early before they become bigger problems.

Accountants – a good accountant should be proactive and be across such matters as the taxation entitlements expats may be eligible for while non-resident.

Financial planners – generally expats are considering the purchase of a property as part of a longer term wealth creation strategy. The purchase of a property may form part of a much bigger wealth creation picture that needs careful consideration. Our preferred planners can provide you on a tailored fee for service basis with quality advice on risk insurances, superannuation, retirement planning and financial goal setting and reviews.

Property managers – you wouldn’t give the keys to an expensive car to just anyone so equally why would you hand over the management of a valuable property to someone you didn’t trust? We have access to some of Melbourne’s best property managers with whom we have had extensive personal experience.

Licensed pre purchase inspections – buying an established property can unearth all sorts of issues, many of which are only found after settlement. Help avoid this situation by requesting an insured pre purchase inspection by one of our selected professionals. Each inspection generates a detailed report covering such matters as structural issues, any unregulated improvements/renovations, asbestos risk and pest infestations.

Our growing expat business is due in no small part to the comprehensive set of services we provide that are tailored to individual needs and involve access to a range of technical and professional skills that are designed to take the hassle out of property investments.

Contact me now to make an obligation free review of your proposed mortgage finance needs on 1300 706 540 or email me direct at [email protected]

Alternatively see my availability & book obligation free skype meeting here.

I’ve been a long term client with Clint and have recommended him to many other clients who have been most impressed. The formation of AXTON has seen service taken to another level – with Bertrand and Richard proving to be top-notch resources – mostly in the clarity and well laid-out instructions in each timely and informative communication they provide. I am living in Canada so the logistics are not simple – however the constant attention and care made the transaction relatively easy. Thanks Guys! Stuart Sandiford – Expat Australian Newfoundland Canada – July 2016